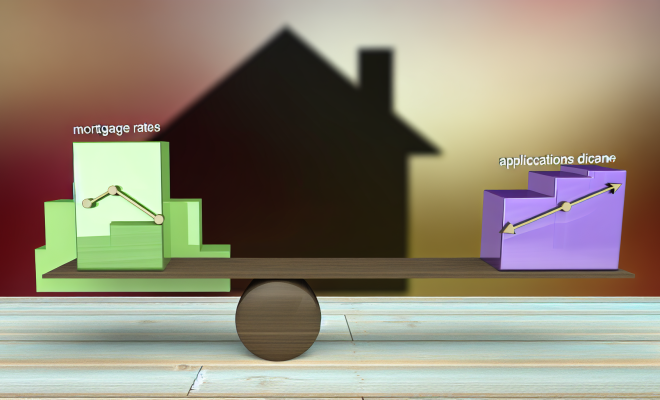

Mortgage Rates Climb as Applications Decline: A Look at the Current Housing Market

The mortgage landscape is witnessing notable changes as we enter the final days of March 2026. According to recent data from Optimal Blue, the average rate for a 30-year fixed-rate conforming mortgage has risen to 6.494%. This marks an increase of 7 basis points from the previous day and a more substantial rise of 13 basis points over the past week.

Understanding the Current Rate Trends

The uptick in mortgage rates is a significant concern for potential homebuyers and those looking to refinance. The 30-year fixed-rate mortgage rate, a popular choice among borrowers, has seen a steady climb, reflecting broader economic trends influenced by various factors.

15-Year Fixed-Rate Mortgages Also on the Rise

In addition to the 30-year fixed-rate mortgage, the average rate for a 15-year fixed-rate mortgage has also increased, now sitting at 5.775%. This rise of 7 basis points over the week highlights a consistent trend across different mortgage products, causing concern among potential buyers.

The Impact of Rising Treasury Yields

One of the primary factors contributing to the increase in mortgage rates is the rise in Treasury yields, which has been significantly influenced by fluctuations in oil prices. According to Joel Kan, Vice President of the Mortgage Bankers Association, higher oil prices have led to elevated Treasury yields, creating a ripple effect that impacts mortgage rates.

- Treasury Yields: The yields on U.S. Treasury securities are often seen as a benchmark for mortgage rates. As these yields rise, so do mortgage rates, making borrowing more expensive for homebuyers.

- Oil Prices: With global oil prices fluctuating, the economic implications are felt across various sectors, including housing. Higher oil prices can lead to increased inflation, prompting a rise in interest rates.

Declining Mortgage Applications

As mortgage rates rise, the demand for mortgage applications has taken a hit. Data from the Mortgage Bankers Association indicates that mortgage applications dropped by 10.5% for the week ending March 20. This decline suggests that potential homebuyers may be hesitant to enter the market amid rising costs.

What Does This Mean for Homebuyers?

For prospective homebuyers, the current economic climate may pose challenges. As mortgage rates rise, the affordability of homes decreases, leading some buyers to reconsider their purchasing decisions. Here are a few implications:

- Increased Monthly Payments: Higher mortgage rates translate to increased monthly payments for borrowers, which can impact budget considerations.

- Market Slowdown: A decline in mortgage applications may signal a slowdown in the housing market, potentially leading to a decrease in home prices.

- Refinancing Challenges: Homeowners looking to refinance may also face higher rates, which could deter them from taking advantage of potential savings.

Looking Ahead: What’s Next for Mortgage Rates?

With economic indicators suggesting continued volatility, the outlook for mortgage rates remains uncertain. Analysts will be closely monitoring the relationship between oil prices, Treasury yields, and inflation rates. Here are some factors to keep an eye on:

- Federal Reserve Actions: The Federal Reserve’s decisions regarding interest rates will play a crucial role in shaping the mortgage landscape. Any moves to combat inflation could further impact borrowing costs.

- Global Economic Trends: The interconnectedness of global markets means that international events, such as geopolitical tensions or changes in trade policies, can influence domestic mortgage rates.

- Consumer Sentiment: Ultimately, consumer confidence will dictate housing market dynamics. If buyers perceive the market as unfavorable, demand will likely continue to wane.

Conclusion

The rise in mortgage rates, coupled with a decline in applications, paints a complex picture of the current housing market. For potential buyers and homeowners, understanding these trends is crucial for making informed decisions. As we continue through 2026, staying abreast of economic developments will be essential for navigating the evolving landscape of mortgage financing.